Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv MONEY With Melissa Francis FOX Business October 29, 2013 5:00pm-6:01pm EDT

5:00 pm

fed plans to begin scaling back. david: we'll cover that live. in addition to being here. "money" with melissa francis is next. we hope to he sue tomorrow. liz: have a great night. >> read my lips, read my lips, no new taxes. melissa: that cost bush 41 big-time. now president obama is having a read my lips moment of his own. what is it going to cost him? this is why money matters. is >> no matter how we reform health care we will keep this promise. to the american people. if you like your doctor, you will be able to keep your doctor, period. [applause] if you like your health care plan, you will be able to keep your health care plan.

5:01 pm

period. [applause] no one will take it away, no matter what. melissa: looks like the president has the some major explaining to do because new reports say that when the president made those fateful comments in 2009, he already knew that at least half the people who buy their own health insurance, were not going to be able to keep their existing plan. politicians had definitely told some whoppers over the years, but just like bush 41's infamous no new taxes promise, president obama's false claim is poised to have hit millions of americans squarely in the wallet. joining us now, are my favorite professor, charles lib some from the university of chicago and igor stroll can i from think progress. thanks for joining us. professor lipton, why these misstatements if you want to call them politely, because they hit people's wallet. it is about your money.

5:02 pm

is that what matters the most? >> that is when it matters the most. the other reason they matter they are flat statements. you can tell when those promises are being broken and one important difference is that when george h.w. bush made that promise, he was making it for some indefinite future. he later broke it about two years later. in the case of president obama, it appears, that he actually knew at the time he was saying it that it was false. but it's a serious problem because people expect the president of the united states to tell them at least what he thinks is the truth. he may be wrong but at least tell us what he thinks is the truth. melissa: igor, isn't that one of the huge problems? buried in the obamacare regulations back in july of 2010 it did say that 40 to 67% of the 14 million customers that buy their insurance themselves, on the individual market, were going to lose their plans, that those plans would be

5:03 pm

eliminateed? seems like now you can go back and prove he actually new that wasn't true? that's a huge problem? >> there are certainly some caveats to his statement but the broad theme of, if you have employer-sponsored coverage -- melissa: that is not what he said. if you have your insurance -- >> that is not what he said. you're right. that is not what he said. melissa: you said you can keep it. now there are millions -- >> hey, i hear you. he should have been more clear. there are caveats. at end of the day, he couldn't have controlled what insurers did, if they decided to change those policies. melissa: but you knew already. not about controlling it. it is about admitting what you already know. >> it is about what insurers do. if insurers decide they will change their policy, if they're not going to follow these new regulations those are decisions they make. melissa: i don't think it is not about not following new regulations. about the fact it is more expensive to cover more people so they're not able to offer individual insurance for $98 a month. >> you're right. they're -- melissa: hang on let professor lip son go.

5:04 pm

>> what igor is doing what you will see a lot of over week or two, shift blame to insurance companies. certainly the case that, insurance companies had to modify their plans in response to the new law. but that didn't mean that the administration couldn't have successfully grandfathered these in. the reason that they put it in such a flat way, with the word, period, nobody will change your plan, period, was that they feared that if they added the caveat that is eyeing gore rightly says they wouldn't sell the program. this passed by the skin of its teeth. every single vote was deciding vote. they just couldn't say the truth, i think and pass it. melissa: igor, if you told people what it would really cost them and meant to their money, a lot of us at the time, if you can do math you can see it just doesn't work out. you can't add these many people

5:05 pm

to the roles especially people who don't have insurance it is too expensive. they have preexisting conditions. put them on for very little money everyone's else's insurance will go way up. if you're honest about the math and money wouldn't have been able to sell it, right. >> the honest answer about the money for most people in the individual market they're going to go into these exchanges and qualify for subsidies, so they're going to get more comprehensive. melissa: that is actually not true. when you look at "l.a. times" article. >> it is true. melissa: case after case. no it is not they have individual case after individual case of people who are -- >> case study one person from california. also states that most people will get subsidies. that same "l.a. times" article. melissa: absolutely not true most people will not get subsidies. >> that is true. melissa: where will money come from? you have to have income level low enough to qualify. that is how you would get it, igor. >> if you're going to ask me a question you have to let me respond. melissa: you have to respond honestly, can't say things factually untrue remain on the

5:06 pm

show. that is my job. hold over one. >> that is your facts. make sure you're telling the truth. or else you can't be on the show. that is the problem. >> look at weighted average of exchanges, of plans being offered in the exchange, it is absolutely true, that six out of 10 people who are going to be buying coverage in the individual market are going to be paying under $100. they're going to be paying less because of the subsidies that are financed by those revenue raisers in the law. that is way law is built. melissa: if people are paying less money how would the math on this possibly work out? >> it doesn't. the problem is, what igor is saying in terms of subsidies, is both benefit of the program and a problem of the program. it's a benefit if you receive the subsidies, so you receive less expensive insurance. but somebody has to pay subsidies. melissa: that always somebody. >> that is paid in the revenue in the law. law is paid for. melissa: we've got to go. thanks to both of you for

5:07 pm

joining us. huge news on zach insider trading saga we've been following forever. adam shapiro is the breaking newsdesk with details. >> yeah. what is new in here is actually kind of old that charlie gasparino, our senior correspondent had been reporting this is kind of deal that could actually be playing out. he reported that over a month ago. here's what is coming down the pike this week, possibly next week, according to charlie, sac may enter into some kind of settlement on criminal issues with the department of justice an pay roughly $1.2 billion fine. it would be largest fine in the history of these kind ever cases, insider trading. when you add already 616 million they have paid in the civil settlement for a previous issue, that is 1.8, a little 1.8 billion. but there are still many questions. if they do announce this as the deal, is steve cohen essentially prohibited from trading other people's money going forward? or would he now then close sac in would he manage his own money

5:08 pm

the key looks as they have they have got a deal. it has not been announced, nobody from the department of justice or u.s. attorney's office in manhattan or sac capital would discuss this issue. according to charlie looks as if a deal is in the works that would result in a $1.2 billion fine and company, not mr. cohen, he has never been charged with anything, keep in mind, but the company, sac would be pleading guilty to the charges against it. melissa: adam shapiro, thank you so much. >> you got it. melissa: so is the key to a happy marriage a shared bank account? a new study says yes. tweet me and tell me what you think. i love your responses so far. some are scary though. it is our "money talker." forget self-service grocery checkout, how about self-service security checks? love it or hate it? we'll show you what it is all about. more "money" coming up. bny mellon combines investment management & investment servicing, giving us unique insights

5:09 pm

which help us attract the industry's brightest minds who create powerful strategies for a country's investments which are used to build new schools to build more bright minds. invested in the world. bny mellon. at od, whatever business you're in, that's the business we're in with premium service like one of the best on-time delivery records and a low claims ratio, we do whatever it takes to make your business our business. od. helping the world keep promises.

5:10 pm

we don't have time for stuff like laundry. we're too busy having fun. we get everything perfectly clean by tossing one of these in the wash. and that's it. i wanted to do that. oh, come on. eh, that's my favorite part. really? that's our tide. what'sours? rask me what it's like to get your best night's sleep every night. [announcer] why not talk to someone who's sleeping on the most highly recommended d in america? ask me about my tempur-pedic. ask me how fast i fall asleep. ask me about staying asleep. [announcer] tempur-pedic owners are more satisfied than owners of any traditional mattress brand. tempur-pedic. the most highly recommended bed in america. now sleep cooler with extra cooling comfort on our bestselling tempur-breeze beds. visit tempurpedic.com to learn more, and find a retailer near you. they're the days to take care of business.. when possibilities become reality.

5:11 pm

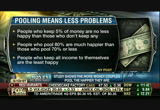

with centurylink as your trusted partner, our visionary cloud infrastructure and global broadband network free you to focus on what matters. with custom communications solutions and responsive, dedicated support, we constantly evolve to meet your needs. every day of the week. centurylink® your link to what's next. melissa: so forget love or communication being the key to a happy marriage because a new study says, what can keep you together is actually the most core are uptive thing out there, money! supposedly spouse that is share a bank account are happier than those who don't.

5:12 pm

do you guys think this rings true? here with today's money talker, jeff gardere, "wall street journal" veronica dagger and celebrity and business powerhouse, jill zare ren. happier couples what do you think? >> 100% happier. i pool my money with my husbands. he has more than i do. now i'm doing okay. but, no, also, it takes one less thing to fight out. one less thing to fight over out of the equation. melissa: really. >> married couples fight about money and power who is spending on what. if you're separate bank accounts, think about this, who is paying for food this week? who is paying for diner? are you paying for diner? those things cause arguments. if it is pooled -- melissa: a lot of people say it is pooled, other person knows who is the big spender is. >> so what? melissa: doesn't that cost -- >> i think you have to use the study. selection bias. work with couples who pool all

5:13 pm

their money are happy like you and your husband. these are the folks who put skin in the game. they're investing investing in r relationship. they trust each other more. more transparency. of course the study will show they are happier. a lot of people have issues with money. money is the bain of many, many marriages. melissa: i wonder, veronica, people keep money separate they have one foot out the door? they have separate bank accounts to make it easier? it is self-selecting the couples that pool it are thinking staying together. what do you think? >> i think you're right. if you're thinking about divorce, thinking of walking away or building a nest egg or not so secret nest egg. you want to walk out the door to pay for a lawyer or what else. melissa: that is ridiculous. if you get divorced half of everything is everyone else's anyway. >> i want to qualify my answer. my mother said, we wrote a book, about secrets of a jewish

5:14 pm

mother. you always have to have your own knipple. which my husband does not agree with at all. melissa: do you, jill? on tv. >> honestly i used to take cash and used to hide it away. i did. this way i wouldn't have to ask him for money or say, i need money to get amani cure. i hate asking for money even though it is my money. melissa: have an atm card, get money for yourself. >> does that. melissa: you don't have an atm card. >> no. credit cards. >> he has most of the money. >> cashless society. melissa: wouldn't know what you were spending money on? >> i did. but then the cash stopped. melissa: that is really comical. >> i think there should be transparency you say listen i have my account, you have your account and pool something in the middle. melissa: that is very complicated. >> my mother is like that. >> you have to have a little bit of privacy. melissa: don't you fight what is coming out of the joint account? i'm doing this out of my account but i want you and joint account

5:15 pm

we pay the rent. >> of course people fight about it. of course they do. of course people fight bit but again, when you have a marriage it is about communication and you try to work out those issues. you win some, you lose some but at the end of the day you compromise. >> having a joint account takes pressure off. you go to wedding and want to buy a wedding gift. i want to spend $300, i want to spend $500. why do we argue about this. i'm in charge buying gifts for family and i go into the joint bank account and buy the gift. melissa: don't you have to have a cfo of the family? in my house that's what you have find. one person who is responsible for keeping track of everything. otherwise people are writing checks out of the same account. >> cfo in most families? women. a lot of guys they turn over, whether the woman is making own money. melissa: not in my house. >> turn it over to the women with wiser about what to do with the money. melissa: are you cfo of your house? >> my mom takes care of everything.

5:16 pm

melissa: a lost women aren't. >> that is the problem. another reason you should have a joint account, if the husband dies, you get a divorce you will be clueless. >> my mother said a lot of woman are in trouble don't have a knipple. end up getting a divorce. melissa: that sounds obscene. >> i can't help it. [all talking at once] >> i'm sorry. melissa: keep saying that. if one person makes the money and controls the bank account, isn't it lop sided in terms of power? >> yes. >> very, very lopsided. if one person makes all of the money, you have to -- melissa: and pays the bills. >> and pays the bills. melissa: even if they toll the other person, do whatever you want i think power -- >> i see a lot of women who resented their partners because of that. that may cause a divorce. you will tell you if you have someone makes all the money and controlling it, you better find something else in the marriage that the other person will be

5:17 pm

must more civil on. melissa: each person has to have own separate accounts, that is being didn't now. that is society. each person has their own rights and do what they want to have privacy. what do you think about that? i don't think my husband needs any privacy. >> no. but my mother, what happened to the old saying, what is his is mine and what is mine is mine? melissa: yes. >> do we like that? melissa: no, i don't think so. >> important to have some sort of independence but have it within the confines of relationship. melissa: you want your cake and eat it too. that makes no sense. how do you make that -- >> 5% of each of incomes spend without checking with the other person. or set a spending limit. melissa: now you're starting to make sense. this is something we said, over x-amount, whatever is comfortable in your household. you can't go out and spend a thousand dollars, say to the other person, how do you feel about this?

5:18 pm

i really want to do this. >> bobby went downstairs for fedex with business but ended up with three boxes from saks fifth avenue, where did these come from? you told me to go on diet yesterday and i already bought this. >> think bull a the money you saved? melissa: i'm growing to leave you guys here to fight about this. >> we are going to fight about that. melissa: come into the home without any cash, because after that segment you don't have any cash. who would not want to do that? which have all the options. plus are you ready for self-service security checks? what the cost of making you feel safe? do you ever have too much money? ? 24/7. i'm sorry, i'm just really reluctant to try new things. really? what's wrong with trying new things? look! mommy's new vacuum! (cat screech) you feel that in your muscles? i do... drink water. it's a long story.

5:19 pm

well, not having branches let's us give you great rates and service. i'd like that. a new way to bank. a better way to save. ally bank. your money needs an ally. help the gulf when we made recover and learn the gulf, bp from what happened so we could be a better, safer energy company. i can tell you - safety is at the heart of everything we do. we've added cutting-edge technology, like a new deepwater well cap and a state-of-the-art monitoring center, whe experts watch over all drilling activity twenty-four-seven.

5:20 pm

and we're sharing what we've learned, so we can all produce energy more safely. our commitment has never been stronger. out for drinks, eats. i have very well fitting dentures. i like to eat a lot of fruits. love them all. the seal i get with the super poligrip free keeps the seeds from getting up underneath. even well-fitting dentures let in food particles. super poligrip is zinc free. with just a few dabs, it's clinically proven to seal out more food particles so you're more comfortable and confident while you eat. a lot of things going on in my life and the last thing i want to be thinking about is my dentures. [ charlie ] try zinc free super poligrip.

5:21 pm

melissa: big thing blocking so many from buying a new home is clearly money, but did you know

5:22 pm

there are ways to pick up a new property without any cash? there are actually some sweet deals for buyers and now, is the time to take advantage, because prices just keep going up. the s&p case-shiller index shows home prices rose 12-point% year-over-year. which is -- 12.8%. large aft annual increase since 2006. real estate expert stan humphries from zillow. i was shocked when i saw the article. yahoo! went out and put together a bunch of places where you can get a loan with almost nothing down. a lot of them are government. veterans administration, no down payment, u.s. department of agriculture, navy federal in virginia. some are private. banks in florida, td a america mortgage. only requires 5% down payment. is this surprising that this is going on now, stan? >> i think a lot of consumers hear that and think 2006 had

5:23 pm

largely gone away the ability to get a large mortgage with no down payment. federal housing administration where you get as little as 3.5%, down, persisted during the downturn and the fact that they have persisted is why federal housing administration mortgages account for 25% of the market place, when people wanted no down payments they had to go to place like fha the trouble with fha mortgages they tend to be a little more expensive for the right to put nothing down. so if you look more like va loan or rural housing service or in a rural community, those have very lowdown payments but, the fees won't be as high as fha mortgage typically. melissa: so, if you're a consumer out there looking at housing market and want to get in and buy something right now. is it smart to go with for one of loans where you don't put anything down, or are there things looking out for? for example, look at td america mortgage. on the surface, looks like really good deal. down payment of 5%. 2% of the down payment can come from outside sources.

5:24 pm

could be a gift. >> yeah. i think that in general, i guess i would caution people. i think these are really good products for first-time homebuyers trying to get into the market to get a foothold and build equity over successive years and equity where they pay larger down payment in the next home. i get a little worried when we see existing homeowners buying next home. melissa: right. >> continue to finance with no cash down. that is exactly what got us into this mess in the housing boom when people were putting nothing down an pulling equity out of their homes through home equity lines of credit. they have no equity. when housing turns down, immediately first to walk away. melissa: right. >> need to be a little bit careful from lender perspective. i think also to be responsible borer, think about how much you should put a little bit of skin in the game. melissa: what you said is exactly what worries me about seeing so many places now cropping up, even beyond the government. we know the government wants to incent people to get out there and buy homes. , for many different reasons. but now if you see private

5:25 pm

lenders actually responsible for their losses, actually doing the same thing, it makes me wonder, are we in another bubble, especially when, beginnings of a bubble, especially when you couple it with the case-shiller data, beginning of segment saying home prices have gone up so much? are we feeling little bit of a bubble right now? >> i would separate the bubble question into, there is what is happening on the lending side and i don't think i would say right now we're in anywhere near, generally lending standards are still quite tight. quite relative to 2006 standards. look longer view they look more like lending standards prevailing in the 1990s. they are not crazy. they are very tight and hard to get a mortgage. zillow analysis last week looking at quotes in the zillow mortgage marketplace, and found a third of americans have less than 620 credit scores, they're getting no quotes whatsoever. so generally those people are locked out of the housing market. when you look at housing bubble,

5:26 pm

more effective ways what are prices doing relative to historical levels. there the u.s. generally looks affordable. for the 15 years before the housing run-up, americans spent 20% of incomes on mortgage payments. right now they're spending 13%. a lot because of low mortgage rates. even if mortgage rates go back up, they would only spend 17, 18% incomes on mortgage, less than half historically. nationally we're not in housing bubble. there are markets look a bit more where the margin is much smaller. melissa: quickly before we go, you said something at the top before, stan. in economics class, if you didn't put money down you were a renter, whether you are a buyer or not. that is what it is about. do people behave differently if they don't put money down when they come into a house or is that a fallacy. >> no, that is distinctly not a fallacy. if you look at two most important factors in default rates, they would be how much money you have put down and what your credit score is. so there is sometimes, you hear this concept, you know, down

5:27 pm

payments don't matter. the empirical data show that distinctly that is not true. more money you have, more vested you are in the house and less like i you are to walk away. melissa: stan humphries, thank you so much. good stuff. >> thank you. melissa: coming up, ready to check yourself in? the idea of self-service security checks may sound scary. could be coming to a venue near you. we'll show you the first of its. "who made money today?" he is helping launch a whole new kind of real estate bond. he is making millions from his midas touch. keep watching to find out who it is. "piles of money" coming up. ♪

5:29 pm

these days i'm living with a higher risk of stroke due to afib, a type of irregular heartbeat, not caused by a heart valve problem. at first, i took warfarin, but i wondered, "could i up my game?" my doctor told me about eliquis. and three important reasons to take eliquis instead. one, in a clinical trial, eliquis was proven to reduce the risk of stroke better than warfarin. two, eliquis had less major bleeding than warfarin. and three... unlike warfarin, there's no routine blood testing. [ male announcer ] don't stop taking eliquis unless your doctor tells you to, as stopping increases your risk of having a stroke. eliquis can cause serious and in rare cases fatal bleeding. don't take eliquis ifyou have an artificial heart valve abnormal bleing. while taking eliquis, yomay bruise more easily and it m take longer than usual for any bleeding to stop. seek immediate medical care for sudden signs of bleeding, like unusual bruising. eliquis may increase your bleeding risk if you take certain medicines. tell your doctor about all planned

5:30 pm

medical or dental procedures. i've got three important reasons to up my game with eliquis. [ male announcer ] ask your doctor today if eliquis is right for you. but it doesn't usually work that way with health care. with unitedhealthcare, i get information on quality rated doctors, treatment options and cost estimates, so we can ke better health decisions. that's health in numbers. unitedhealthcare. ♪ melissa: the grocery store checkout, customer service tollbooths kamal services now being handled by machines. coming soon, security check in.

5:31 pm

a california start up we will start offering automated security checkpoints as like stadiums and amusement parks. make sure that the airport's security line won't be far behind, the woman behind the technology, founder and ceo. thank you for joining us. tell us how it works. >> well, thank you very much for having me on the show. the way that this works is, this is really a whole entry experience solution. it puts together different technology and processes. what you do is walk up to this really beautiful honeycomb looking system and see a green door. he would take your ticket or your boarding pass or your insurance card, whatever it may be for that they swipe it to open the door and place your bag in sight. then you would walk through whichever date or detection mechanism is already there at the venue.

5:32 pm

in the meantime the system as multiple sensors that are all looking for hundreds of parameters, calculating. everything is okay you will take your bag out. you will be the only one that. melissa: one of the biggest differences for people that are experiencing it is rather than putting your stuff on the belts where it goes through and they're is a human being looking at the monitor and deciding whether or not there is something in your bag, hear a computer is deciding what they're not their something in your bag. you say the point is not simply to match a knife in your carry-on are back with a knife that is in the database, but rather for the computer to understand what a knife is a detective. what does that mean? >> well, what it means is that -- is that this computer understands. we teach it what a threat is and what a family affair is which is important because you don't want to be looking for yesterday's problem. you want to be able to find something new and different that you have not exactly seen before

5:33 pm

and by being able to keep everything in the bank. melissa: how does it do that? algorithm, heat, how? >> it uses multiple sensors and calculates based upon the sensors these teaches. it is called machine learning and the machine basically learns this phenomenon. melissa: it looks like it will be cheaper than having a normal x-ray machine, takes up less to have less space, a quarter of this base. 50 percent less staffing. how much do you save on average, and is that one of the big selling points? >> well, most definitely if you will be getting down the cost of your personnel by 50 percent or even one third you will be seeing annually large personnel and operational costs. usually with equipment like this , service contracts also cost. our security service makes all

5:34 pm

of that, but it all into one package -- melissa: how is the basic machine compared to a built-in scanner that we would see if the airport? cheaper, more expensive? >> well, it is entirely unrelated because we're putting together an entire suite of security services that also include connecting in talking to other systems and all those services that go around it. there is no way to compare. melissa: one cost some amount in the other, something else. is it more expensive but you're saying you give more? >> the way you might compare it, if you wanted to take someone using a technology already in place to replace five lanes you would be able to save anywhere between m million to even two per year on the total package of what needs to be around the systems. melissa: your first batch of centers, five of them, already spoken for.

5:35 pm

obviously demand. thank you so much for coming on. appreciate your time. >> thank you. melissa: you have seen what it is all about. is it easier to outsmart a machine and a person? a former new york city police detective and security expert. what do you think? >> are undertaking is ambitious, but i have three serious questions. the first is, she earns and that the machine will learn a cumulatively as it gains intel and data it will give more efficient. my first concern is the learning curve. does it take six months for it to become smart enough to know that the knife is a knife, not a series of of rhythms, as you referenced, which is kind of what is real and lakes is about, an anomaly of pixels in the picture. melissa: i have to say to my just a computer to look eerily throwback better than i just a person, you know, it may be midnight, it may be that they are tired. distracted, we have all gone through security, whether the tsa or a stadium.

5:36 pm

i go through a stadium. i mean, it's a huge target. they barely check your bank. they let you bring less and less income will you bring in, the pad down is basic. even if they're is a learning curve i tend to adjust the machine more. am i wrong? >> i would tend to part company with you. my first point would be one not both. melissa: with a polite way to disagree. >> there is more that came from. the thing is, what about weapons that are not house in traditional bodies. for instance, knives that are belt buckles, handguns that us here at letters, that machine will not learn that in kelp -- until it encounters that anomaly. melissa: when the human misestimated? >> i've not think so. properly trained personnel who are nosey and inquisitive and thorough -- in on the same alar, a properly trained personnel will identify that. why not both? melissa: but the other problem. you were busy writing. what else bothered you?

5:37 pm

>> i was writing down nice way to disagree with you. trick weapons, a cumulative knowledge, and the fragility of the circumstances the thing is this, if an airport check-in line is 65 degrees and it is chilly, the air-conditioning is on and someone is sitting on line and sweating profusely and agitated and nervous, that totality of factors, disparate factors, a human being will subjectively process and say to my guess what, she looks a little suspicious inclined to look closer. melissa: the human element, the debt and steve, this person gets me a feel. i don't really trust. she is saying no. especially if you look and airports situation, this is not the scanner that the person goes through. this is for the bag. you wonder in combination if you have this on the com system that you showed a switch that is where you put your bag, you kirk fear -- to you think not having

5:38 pm

human beings look inside the bag and all, is that a better situation? worse, the same? >> net-net, worse. the reasons i have outlined some of the totality of factors. it helps the process. the database will not have those records. they may not have about -- belt buckle that is a hand gun or knife that is a cigarette lighter and the other one is quite honestly that this machine is objective. it is waiting for a change in pixels, the same as video analytics. melissa: he thinks objective is better? >> absolutely. melissa: interesting. from the u.s., every -- money has been flying around every corner of the globe. struck a deal with the chinese company to start offering home theaters. the latest sign of a powerful lure that china has become for hollywood and its suppliers. the deal was made because it expects china to be the biggest market for home theaters. the new system, get ready for

5:39 pm

this, $250,000. next to cuba the un general assembly is pressing for the 22nd time for the u.s. to end its embargo against the country. china's foreign minister says the american policy which has been in place for 53 years is barbaric and amounts to genocide . the economic damage has caused more than a trillion dollars. 188 countries voted for lifting the embargo. is row was the only country that join the u.s. and voting against it. and over to russia where the country has broken in zero ways to pledge for the upcoming olympics it was the centerpiece of russia's bid to host the games. it pross the cleanest olympics ever by not dumping construction waste. the associated press went for a visit and reports that tons of construction waste is being dumped in an illegal land fill. that could even possibly contaminate the water were the gains will take place.

5:40 pm

evidently russia's budget did not provide a full treaty construction waste. next up, tiger taken out. the newest p.g.a. golf tour video game will not include them. he is just not "money" enough. wait until you hear the details. the end of the day, i guess it is all about birdies. ♪ [ male announcer ] it is more than just a new car... more than a new interior lighting system. ♪

5:41 pm

it is more than a hot stone massage. and more than your favorite scent infused into the cabin. it is a completely new era of innovation. and the highest expression of mercedes-benz. introducing the 2014 s-class. the best or nothing.

5:42 pm

introducing the 2014 s-class. at od, whatever business you're in, that's the business we're in

5:43 pm

with premium service like one of the best on-time delivery records and a low claims ratio, we do whatever it takes to make your business our business. od. helping the world keep promises. ♪ melissa: it looks like it is game over for tiger woods, video-game giant electronic arts has cut ties, opting to leave him completely out of the pro golf pga game that has worn his name for the past 15 years. it is a sign that his off the course dalliances and declining play have finally caught up with his brand? in sports marketing strategist. i mean, is this shocking to you the you have a golf game without tagger in a?

5:44 pm

>> not really. if you look at the fact of why people on buying, it's because they make a really good product. the fact that tiger woods, it will be tiger woods pga tour golf, people and not going to not buy it. melissa: my first thought was it's all about the money. they don't want to pay him. is it that or is it that he just carries too much baggage? >> at this point people look at this as an active thought. a tie him up with the gossip, but the fact is he is winning on the golf course, but not winning majors which is what people really plays into when they think of tiger woods. he has not done it, so he is not as marketable. melissa: a cautionary tale. i mean, and of course i want to make the point that he is not going to miss this. he is still the highest paid athlete out there. i'm sure he could care less, but is it a cautionary tale for others who are letting their brand slip? who was to uc in danger of being dropped from being a headliner?

5:45 pm

>> i think that if you look at like a boxer, for many years the tiger was a boxing, indestructible. then you lose one fight, dump floyd may weather for a little bit. all this and you are not as marketable. tagger had problems of that range, but he also had them on the range and had not been performing at the same level. melissa: 8-run is another example. >> in no way. he never had the endorsement dollars. if you look at overall salary he was always in the top ten because he was the highest-paid baseball player, barely dragging a million in endorsements. .ow or never went to him for a melissa: michael vick. somebody else. is it possible -- he is somebody who people watch him again. you never thought -- i was not sure you would never see him play again. could he ever reclaim endorsements? >> it would be tough because when you're dealing with dogfighting, that is something

5:46 pm

that is hard to come back from, and he is not performing on the field. who he should look at is kobe bryant. great charges, different things that went on, major indoor surfers bright, nike, and the face of the nba along with lebron james. in terms of coming back from scandal it is really covey bryant is set to stand did. melissa: back to tiger woods. is it about the play or the gossip? if he was to get back, you know, if that is impossible. >> if it is even possible. melissa: the invincibility that he had before, even half of it, would he be right back in? or is the branch is tired? >> think the brand is tired and they're looking to go in a different direction. what this opens up is going to a competitor in helping to brand the competitor's new game and really getting a bigger piece of the pie, may be having more creative input. it would be if another game developer could brand their game with him. that would be something to look

5:47 pm

for. melissa: interesting. would you pay big dollars for art on an ipad? an exhibit filled with images made on an application. is it art? what do you think? look at that. is that our? stay where you are for "spare change." you can never have too much "money." ♪

5:50 pm

♪ melissa: it is time for a little hard fine in "spare change." a whole new medium of art created with an act on an ipad. britain's most celebrated living artist has a new exhibit at the fine arts museum of san francisco on display. 147 pieces that huckabee created on his ipad and 18 that he made

5:51 pm

and is iphone. most of the pieces are displayed on a digital monitor like these, but some of the works of been printed out in their 12 feet tall, like these, you simply national park. joining me now, the deputy director of the fine arts museum of san francisco, richard. thank you so much for joining us. what is your response to critics who say it is not art? >> well, i would beg to differ with them to start with. david hockney has been interested in technology his entire career and has been making all sorts of prints. i think that this ipad technology and the ability to draw on the ipad is taking him into that next phase. as he says, it is a new medium, and we don't know where will lead, but the one thing that he is doing would be drawings that he does on the ipad to my very similar to what he has done

5:52 pm

throughout his career. he is printing them, as you said, the bigger drawings are printed 12 feet high. he is using a very high-quality ink jet printer that takes 20 minutes for each sheet to printout. he is really pushing the limits of the technology in every direction. the ipad does not draw itself. you have to be a great artist to produce the sorts of things that he has done on the ipad. and, of course and he is pushing the limits of the printer. melissa: i understand the uses his index finger to paint instead of a brush. it is obviously different from blending wiles of watercolors. you know, how -- can you explain how you get the different pigmentation an intimation of color if you're using your finger rather than a brush and actual physical material? >> right. i have not done any myself, but my understanding is he's using

5:53 pm

an act called brushes on the ipad. and that allows them to select from a huge array of colors and also to makes the colors, but also allows him to adjust the width of the line that he makes with his finger as well as the different effects, whether it is a brush-like effect. and he actually cause -- calls it drying on the ipad, not painting. and that is a big distinction. melissa: it is. i can see what you're saying. to us it is large and colorful, as they have to think about amateurs are being educated. it seems synonymous with the painting because it is -- that is how it looks like people of doing it in the facility. of course of our is priceless. our show is called "money" and we are all about "money." as of right now is it worth more or less right now?

5:54 pm

you would know. you can sure these things. is it worth more less right now? >> i don't want to talk about the price of art because in the museum field we are all very reluctant to do that. will say that david has not sold any of these drawings that are printed get. so it remains to be seen but the market will be for them. however, he is still pointing. when he returned to california in july he started painting in acrylic on while, portraits of his friends and close ones, and we have 18 of those. that young museum in golden gate park where the exhibition is on view. melissa: i am sure it is phenomenal. i looked at the work on line. it is breathtaking. have been to the museum. thank you for spending your time with us. we appreciate it. >> in queue for having me on, and come csn san francisco. melissa: for sure. up next, who made -- today. one of real-estate sand used

5:55 pm

billionaire bowles. i will tell you who it is right after this. you can never have too much "money" 42 much art. ♪ so ally bank has a raise your rate cd that wothat's correct.a rate. cause i'm really nervous about getting trapped. why's that? uh, mark? go get help! i have my reasons. look, you don't have to feel trapped with our raise your rate cd. if our rate on this cd goes up, yours can too. oh that sounds nice. don't feel trapped with the ally raise your rate cd. ally bank. your money needs an ally.

5:58 pm

♪ melissa: whether it is on wall street on main street, here is to make "money" today. everyone who owns blackstone group. to hedge fund is preparing to sell half a billion dollars in rand backed securities, similar to mortgage-backed securities, but these bonds are backed by monthly rent paid they allow a transfer of risk from blackstone to bondholders. investors are liking what they hear about that. the stock closed up more than three and a half% today. jonathan gray collins 40 million shares of the company. that means he made thirtysomething million dollars today. very nice. all right. and finding forgotten money.

5:59 pm

a guy in norway who bought about $27 worth of bids : back in 2009, he was writing a thesis on encryption. he then forgot all about it until the widespread media coverage. when he checked on his investment he calculated that it had turned into a windfall of an amazing 806,000. and i get excited when i find it tandon bill in my jacket. throwing "money" away, this guy went to the mat to prevent his ex-wife from getting any money in a divorce. he told the judge that he converted their life savings of $500,000 into gold, about 22 pounds of it. he then down to it in the trash. the 22 pounds of gold. i'm not even sure i believe that story. that's all we have for you. we hope you made "money" today. be sure to tune in tomorrow. barbara corcoran will be here to

6:00 pm

talk about making money from food trucks. plus, i got in one to learn the tricks and the trades. don't miss that tomorrow. it will be awesome. "the willis report" is coming up next. ♪ gerri: hello, everybody. i'm gerri willis. tonight on "the willis report" the obamacare rollout mess, when did the president know that millions of americans would be kicked off their health insurance plan? despite his repeated assurances to the contrary. >> if you like your health care plan you will be a will to keep your health care plan. gerri: also, a preview of kathleen sibelius' congressional testimony tomorrow, the head of the committee, chairman fred upton is here. finally, and apology on the obamacare rollout. >> i want to apologize to you that these website has not worked as well as it should. gerri: will the site ever work for consumers? we're watching out for you

74 Views

IN COLLECTIONS

FOX Business Television Archive

Television Archive  Television Archive News Search Service

Television Archive News Search Service

Uploaded by TV Archive on